Dear Friends,

I have been hunting for an interesting topic and I saw an email from my friend and well-wisher Muthu, which made me chose this topic of returns from various asset classes.

While it’s a universal truth that returns from Equity beats all other asset classes in the long run, I have had innumerable discussions with people on the volatility that is inherent to equity investing and returns that we can make for anxiety that it causes to some. One thing that is clearly evident is that there is “No Gain without Pain” and returns are proportional to the risks that we take.

I want to quote what our “Ulaganayanan” Kamal Hasan mentioned in one of his interviews that I happened to tune into. It goes something like this:

“When you start body building by going to a gym, the body starts paining a lot and quite a number of people drop the idea unable to bear it. It’s not just the pain associated with body building but the priorities also keep changing and we tend to discontinue the process. For people who have not hit the gym, walking for a long time, and climbing hills as a one off case will also result in body discomfort and the leg muscles pain for a few days. The reason why the body pains is that, the muscles get toned but we need to continue exercising meticulously to get to a good physique – No Pain No Gain”

Likewise, Equity investing might cause some anxious moments in the short term but the wealth creating ability of equities is too good to ignore.

I have presented some interesting facts that are sourced from various websites and research papers including RBI, BSE, and Money Control.

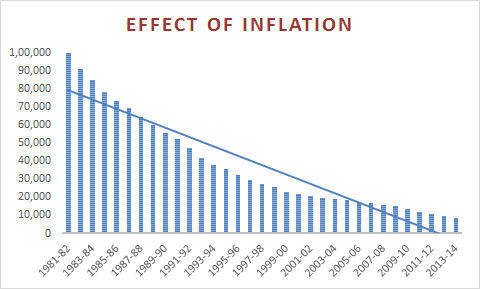

The graph below depicts the effect of Inflation in the long run. The value of Rs. 1 lakh in 1981-82 has become Rs. 8,819/- i.e. Rupee lost its value by 92% due to inflation.

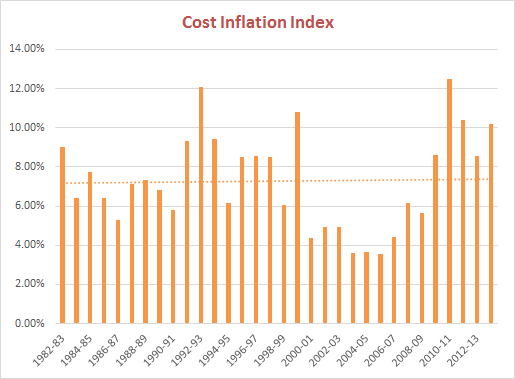

I have chosen the period of observation from FY 1982 when government started publishing the cost inflation index (CII – This is the figure that we use for indexation benefits). CII value was 100 for FY 1982 and has gone up to 939 for FY 2014 – a whopping 939% in 32 years, approx. 7.3% on an Annualized basis. The yearly numbers vary from as low as 3.54% in FY 2006 to as high as 12.5% in FY2011 (NDA 2 period when Inflation was skyrocketing). The value CII value is 939 for FY 2014 and the percentage increase over previous year i.e. FY 2014 over FY 2013 is 10.21%.

The following are some of the questions that keep cropping up on a regular basis from various investors:

- Is Equity Investing a gamble?

- Will I make money investing in stock markets?

- I don’t want to take any risk and invest in safe assets like Bank and Post Office deposits

- How much of returns can I expect from Stock Markets, Gold and Real Estate?

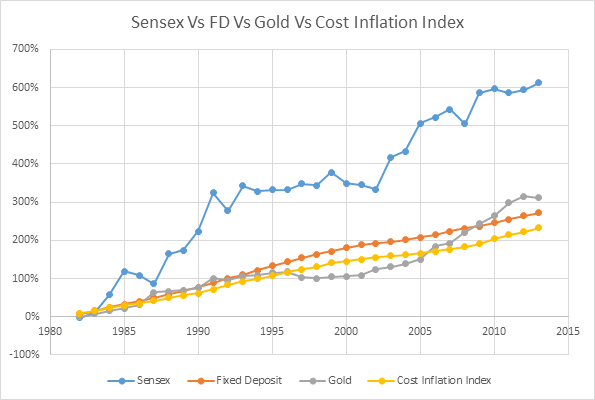

While I am not getting into answering the above questions (some are already addressed in the PenguWIN Website https://penguwin.com/ask-penguwin), I want to present my views based on the comparison chart below that addresses these questions.

- Equity and Real Estate are the asset classes that can give real returns in the long term. If the inflation is 8% and if the nominal return from an asset class is 10%, then Real return would be 1.85%: ((1+Nominal Return)/(1+Inflation) – 1))

- Returns from Bank and Postal Deposits, Gold (Gold had a tremendous run for some time), company deposits etc. barely manage to cope up with inflation or even less most of the time resulting in investment value going down. You can see that the cost inflation index, fixed deposits, gold are almost even.

Asset Class |

Investment in 1982 |

Value on 31Mar’14 |

% Returns |

Equity (Sensex) |

1,00,000/- |

2,23,86,000/- |

19.16% |

Bank Fixed Deposit |

1,00,000/- |

16,94,000/- |

8.52% |

Gold |

1,00,000/- |

36,51,000/- |

9.75% |

- Only Equity has been successful in withstanding the onslaught of Inflation and has given a real return of over 10%, adjusted for inflation. 1 lakh invested in Indian Equity in FY 1982 is worth Rs. 2,23,86,000/- (2.24 Crores). Please note that these are just returns from Sensex and our active mutual fund managers generate a handsome alpha over and above this in the rage of 5+% compared to Sensex.

Does this mean that all our money has to go into equity? No, the point is that equity has to be an integral part of the portfolio to ensure that the overall portfolio return is able to beat inflation. The stability that the Fixed Income provides is very essential and that is the secret sauce of asset allocation that is widely talked about.

Please do send me your comments to [email protected] and share your views on my blog. I would also request you to send me some interesting topics that you want me to blog on and if it’s an area of my expertise, I will definitely take it up.

Blog #PenguWIN 1002 – Historical returns of Stocks, Gold, and Fixed Deposit Assets compared to Inflation in India