Dear Friends,

Most of us typically run around for Tax Saving options during the months of Dec, Jan and Feb to exploit section 80C benefits and minimize taxes.

There are a plethora of investment options under Section 80C including:

- Employee Provident Fund (EPF – company deducts this through payroll and this is an amount that everyone in organized employment saves),

- Public Provident Fund (PPF),

- 5 Year Tax Saving Bank Fixed Deposit,

- National Savings Certificate (NSC),

- Life Insurance Premium payment,

- New Pension Scheme

- Home Loan Principal Payment and

- Equity Linked Savings Scheme (ELSS) of Mutual Funds.

From last financial year an additional contribution of 50,000/- can be made to National Pension Scheme (NPS) under 80CCD based on the recommendation of Finance Ministry. Out of 1.5 Lakhs, EPF is mandatory and gets deducted as part of the payroll. So the available amount for additional investments is 1.5 lakhs – EPF. This amount will be further reduced if you are paying a home loan and the amount of principal repaid can be deducted from this 1.5 Lakhs.

Among the options available for savings through 80C, ELSS is an excellent choice, especially for people in their early stages of career. Following are the reasons to go with ELSS:

- Allocation to equities is extremely important for long term wealth creation, and earn handsome inflation adjusted returns. ELSS provides an option to achieve this objective, especially for people who have limited investable surplus and get the dual benefit of tax savings plus equity investment

- The lock in period for ELSS is only 3 years which is the minimum among instruments available under 80 C exemption.

- Since ELSS is equity investment, dividend and capital gains returns are completely tax free.

- Indian economy is on the revival path with a stable government, decreasing current account and fiscal deficit, policy reforms, decreasing inflation, improving GDP and earnings forecast etc., and all these augur well for good equity market performance in the long run.

- In open ended Mutual Funds, the fund managers are constrained by redemption challenges. The flows are better controlled in ELSS Mutual Funds due to the 3 year lock-in and hence gives them better manoeuvrability for generating additional returns.

- At current levels both Sensex and Nifty are undervalued from long term averages and makes it a good entry point for Investors Long Term Wealth creation

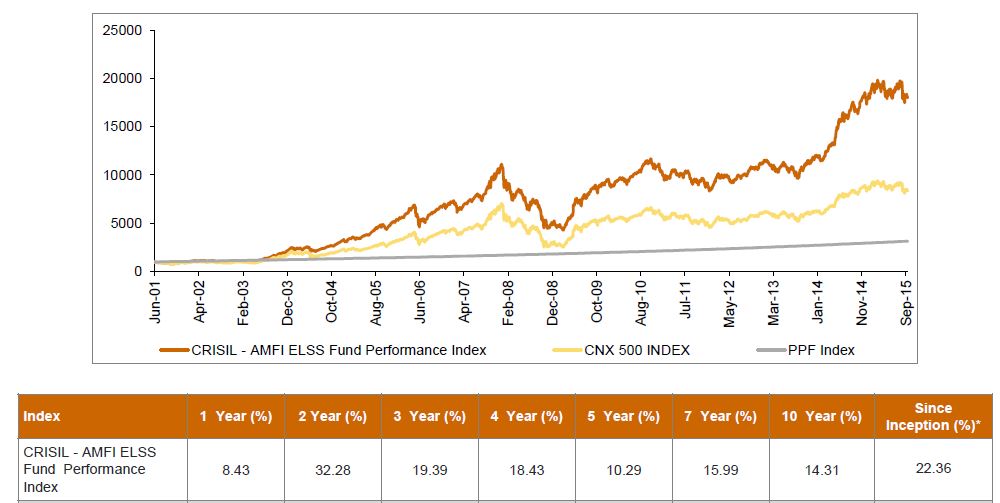

The CRISIL – AMFI ELSS Index (Taken from CRISIL Website) is presented below as of Sep 2015. The returns are quite exciting @22.36 CAGR since inception

The following table gives the long term performance of key ELSS Funds, returns are CAGR (Compounded Annualized Growth Rate)

| ELSS Fund | 1-Year Return | 3-Year Return | 5-Year Return | 10-Year Return |

| Axis Long Term Equity Fund | 8.18 | 25.97 | 18.61 | – |

| Birla Sun Life Tax Relief 96 | 11.15 | 21.99 | 12.08 | 14.13 |

| BNP Paribas Long Term Equity Fund | 7.81 | 20.29 | 14.72 | – |

| Franklin India Taxshield Fund | 6.72 | 19.95 | 13.62 | 15.52 |

| ICICI Prudential Long Term Equity Fund | 6.01 | 19.75 | 12.77 | 14.02 |

| IDFC Tax Advantage Fund | 8.92 | 19.3 | 12.48 | – |

| Reliance Tax Saver Fund | -0.37 | 22.06 | 14.95 | 15.05 |

| Religare Invesco Tax Plan | 7.34 | 21.06 | 13.54 | – |

<Blog # PenguWIN 1039 – Taxing Time>

Your blog is informative